Affordable rental housing has many of the same cost components as market-rate housing: land, development fees/taxes, labor and materials, and soft costs. However, affordable housing often has higher costs of development due to requirements placed on homes built with public subsidies. This includes prevailing wages for construction workers and additional environmental requirements. According to the Terner Center at UC Berkeley, affordable housing developments “are often subject to increased local scrutiny, further inflating costs.” The 2014 study found that local government design requirements for affordable housing added an average of seven percent in total costs, and that community opposition (measured by holding four or more community meetings) increased expenses by five percent.

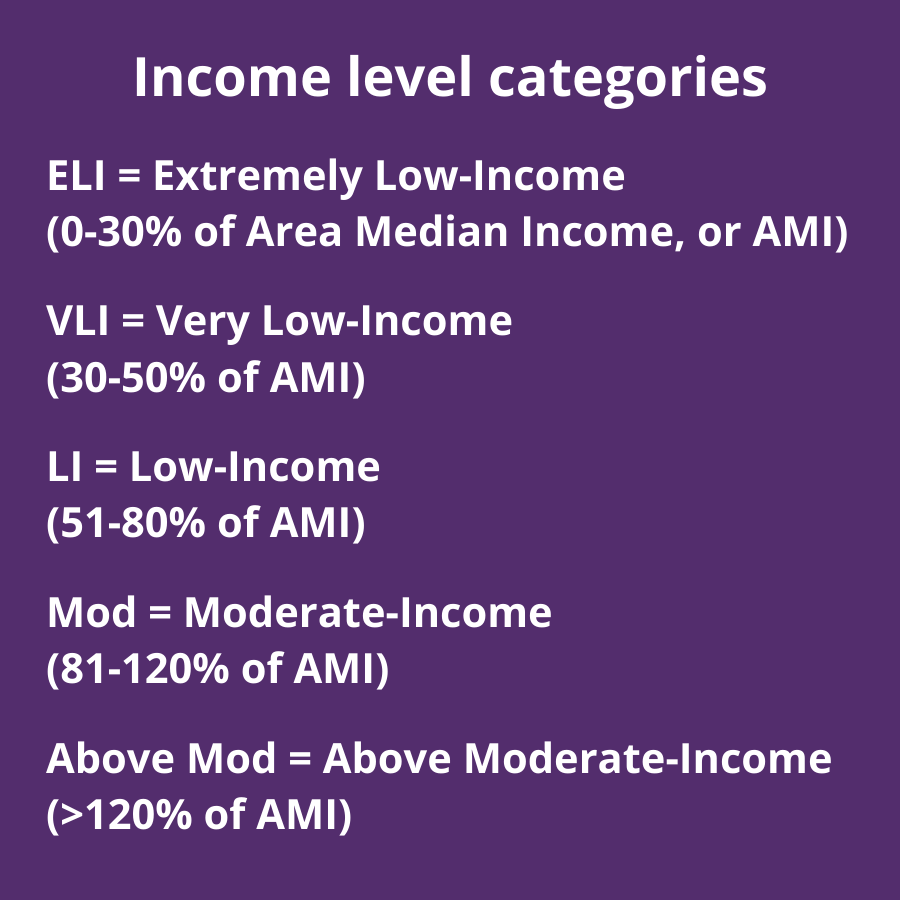

Traditional deed-restricted affordable housing limits who is eligible to live in a development and what rent they will be charged based on the level of household income and the number of people living in the household. The income level categories are established by the Department of Housing and Urban Development (HUD):

Eligibility is determined by percentages of area median income (AMI) by household size. Rents are established at no more than 30% of various percentages of AMI (not necessarily just at the upper limit of the ELI, VLI, and LI income categories), varying by unit size.

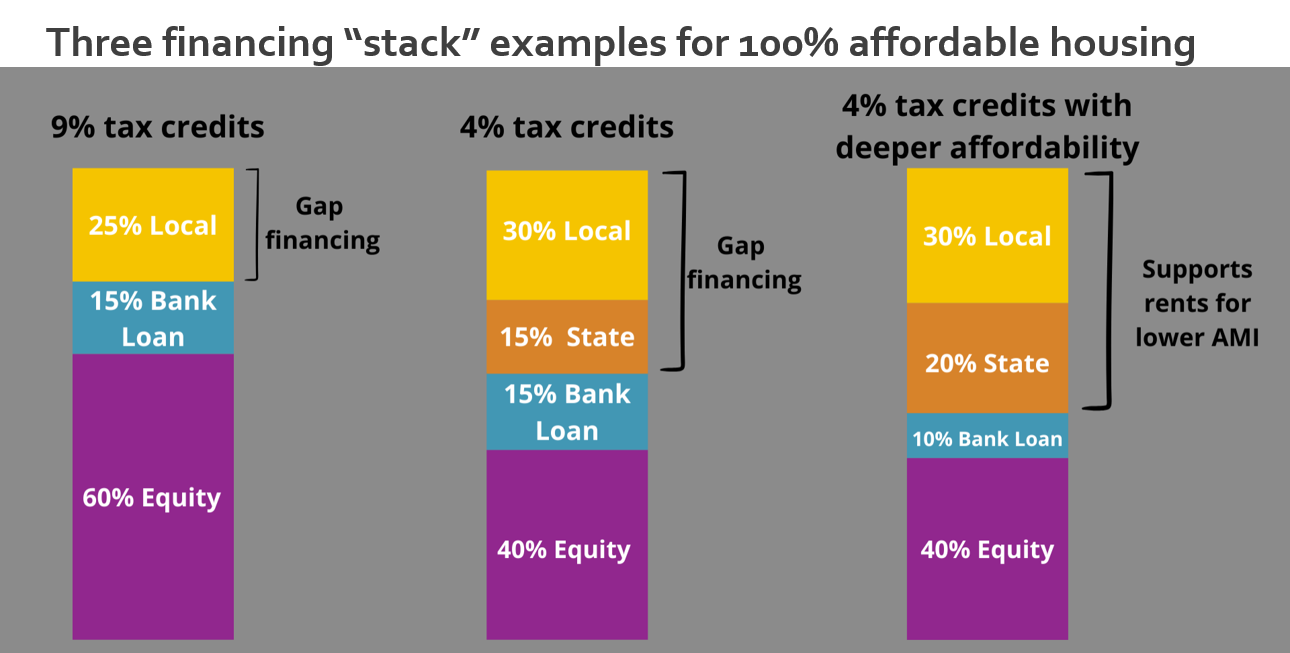

For traditional affordable housing development, the revenue stream from rents cannot support the same level of debt from private lenders that can be supported by market-rate rents, so loans are smaller. These loans come in two forms: a 30-year mortgage from a bank or other commercial lender at market-rate interest (typically somewhat higher than is available for homebuyers); or a somewhat larger loan in the form of the proceeds from a bond issued by a public agency at an interest rate about 1% lower than those of a commercial bank. Market-rate housing developers can obtain long-term mortgage loans from commercial lenders, but currently need to contribute at least 25% of the total project cost in the form of equity.

Because the private lender loans are smaller, there is a funding “gap,” which is typically filled with multiple different funding sources. Virtually all of these subsidy sources adopt thresholds for funding, such as depth of income levels to be served, locational criteria, age, and disability or homelessness status. Low-interest loans with very favorable repayment provisions (known as “soft money” loans) as well as grants are made available by cities, the County, and the State. Forgivable loans are provided by the Federal Home Loan Bank. The U.S. Department of Housing and Urban Development provides forgivable loans for projects serving certain populations. Low-Income Housing Tax Credits are invested in projects in the form of equity that does not need to be repaid. The Housing Authority can provide operating subsidies in the form of project-based Section 8 vouchers.

Only a relatively small part of the affordable housing development financing stack is from local money. Multiple state funding sources each have their own timeline and requirements. Developers also need a commercial bank loan to cover a portion of the costs. Loan underwriters must consider the property’s cash flow when deciding how much to loan, so if units are being offered to families a the lower income levels at lower rents, the developer will receive less money in the loan. The lower the income level, the lower the loan. There is still a gap left over after the developer has lined up tax credit financing and a commercial loan. The remaining gap needs to be made up with local money from cities or the county. That could come from a range of sources.

Affordable Housing Funding Sources

Click the source of funding below to learn more about each one.

Cities

For those cities in Santa Clara County that finance affordable housing development, each has its own ways of raising revenue that is used for financing the development of affordable housing. Each city will have some but not necessarily all of the sources listed below. Please note that this listing uses generic titles in some case, so a city may have such a listed funding source called by a different name.

- A commercial linkage fee is a type of impact fee that can be charged based on an assessment of the extent to which new commercial and/or non-residential development generates additional demand for affordable housing. Typically, the fees are based on the square footage of the development and vary by type: offices; hotels; retail stores; industrial space.

- A housing impact fee is similar to the commercial linkage fee but is charged on the development of market-rate housing. It is also charge on the square footage of the project. Most cities which had this fee on the books have discontinued it since inclusionary housing requirements on rental housing became legal at the beginning of 2018. Fees collected in the past – or repayments on loans made from this source – will continue to be a source of financing into the future.

- For cities that have inclusionary housing requirements, they must also allow the payment of in-lieu fees rather than providing the affordable units. These funds can be invested by the city into affordable housing.

- The State of California imposes fees on the recordation of documents associated with certain real estate transactions, commonly known as Senate Bill 2 (SB 2) Starting in 2019, the revenue is being shared, by formula, between the State, cities and counties.

- Larger cities receive annual entitlement grants from the U.S. Department of Housing and Urban Development (HUD) from the HOME Investment Partnership Program, under which affordable housing development is an eligible use. Those cities also receive entitlement grants under the Community Development Block Grant program – CDBG – which can be used to finance some expenses of development.

- Many cities offer fee waivers or discounts on some impact fees — parkland dedication in-lieu fees, for example – for housing developments that will serve certain lower income levels.

Santa Clara County

The County administers funds raised by the sale of general obligation bonds authorized by Measure A, approved on the November 2016 County-wide ballot. Out of the total of $950 million of authorized bonding, at least $800 million is allocated to multifamily rental housing developments. The housing funded from this source must be targeted to certain populations, including veterans, seniors, disabled persons, victims of abuse, the homeless, and individuals suffering from mental health or substance abuse illnesses. Funding to individual projects is made in the form of soft-money loans. As of mid-2019, the County had approved loans totaling $205,030,000 to 16 new construction projects (totaling 1,418 units) and $29,150,000 to rehabilitate two existing affordable housing properties (totaling 481 units).

Housing Authority of the County of Santa Clara

The Housing Authority can provide an indirect subsidy to an affordable housing project by providing project-based Section 8 vouchers. For the units with such vouchers, the normal affordable rent level plus the extra subsidy provided by the voucher means that the developer will receive more revenue than would otherwise be the case. This, in turn, allows the developer to borrow more funds in the form of either a tax-exempt bond or a conventional commercial loan.

State of California

The Department of Housing and Community Development (HCD) administers the State’s several funding programs that are available to affordable housing developers. HCD does not permit any one development to receive funding from more than one of these programs.

- The Affordable Housing and Sustainable Communities program, or AHSC, funds compact development in infill projects that will reduce greenhouse gas emissions. Local Governments can use the funds towards affordable housing developments, housing related infrastructure, and sustainable transportation infrastructure. Funding awards are the result of a competitive process. In 2019, $31.5 million was awarded to two projects in San Jose.

- The No Place Like Home program funds developments that will house persons who are experiencing chronic homelessness or who are at risk of chronic homelessness, and in need of mental health services. The County of Santa Clara has been awarded $20,478,901. Developers will need to apply directly to the County to receive funding.

- The Veterans Housing and Homeless Prevention program, or VHHP, funds housing for veterans of the U.S. armed services and their families. In 2019, $75 million was allocated to the program, though none had been awarded by mid-year. Not less than 15% of the funds must be awarded to projects in Alameda, Contra Costa, Marin, San Francisco, San Mateo, Santa Clara, Santa Cruz and Sonoma Counties.

- Multifamily Housing Program, or MHP, funds new construction, rehabilitation, and preservation of permanent and transitional rental housing for lower income households. The funds are a permanent funding source available for post-construction costs such as social services associated with housing units, property acquisition, refinancing to maintain affordability, building improvements. A $1.5 billion general obligation bond was authorized by the State Legislature in 2018; a NOFA for $178 million in the first round of funding was issued in June 2019. There are no formal regulations that allocate potential funding awards by region, though HCD is known to have informal, internal guidelines to ensure that MHP funding is fairly distributed across the State.

- The Supportive Housing Multifamily Housing Program, or SHMHP, funds are available for permanent affordable rental housing that includes supportive units. Eligible projects include 5 or more units with associated supportive services. In 2019, $155 million was allocated to the program, though none had been awarded by mid-year. Awards will be the result of a Statewide competitive process with no regional allocations.

Private Sources

Private funds are invested in affordable housing in three ways:

First, affordable housing qualifies for funding using private-activity bonds issued by public agencies. The private entities who buy these tax-exempt bonds pay about 1% less than the going rate for a mortgage from a commercial bank. By federal law, there is a limited amount of private activity bonds that can be issued every year, and that amount of authorization is divided between the states on a population basis. The California Debt Limitation Allocation Committee (CDLAC), staffed by the State Treasurer’s Office, administers the State’s authorization allocation. If demand for bonding authority is relatively low, it can be relatively easy for developers to get an allocation through an over-the-counter process. Due to high demand for bonding authority, CDLAC made awards a competitive process in 2019.

- 9% tax credits provide the greater percentage of project cost and are highly coveted. Funding rounds are extremely competitive and some projects have to be submitted several times before receiving an award. 9% credits cannot be combined with tax-exempt bonds. TCAC has established allocations by region; San Mateo and Santa Clara Counties comprise one such region, and can be awarded no more than 6% of the total awards in any one funding round. As of mid-2019, it had been more than two years since any project in Santa Clara County had received a 9% tax credit award.

- 4% tax credits finance a smaller percentage of project cost, and used to be automatically available to projects that receive a tax-exempt bond allocation. However, due to demand that exceeds the federal cap on total tax credits that be awarded annually by the state, 4% tax credits are now competitive.

Second, the California Tax Credit Allocation Committee (TCAC) administers the low income housing tax credit (LIHTC) program to encourage private investment in affordable rental housing for households meeting certain income requirements. Credits are available for new construction projects or existing properties undergoing rehabilitation. Projects compete on point scoring, but because most projects receive the maximum point score, TCAC’s tiebreaker formula generally decides the outcomes. Low-Income Housing Tax Credits are features of both federal and State tax codes.

The program awards developers federal tax credits to offset construction costs in exchange for agreeing to reserve units that are rent-restricted and for lower-income households. The credits are claimed over a 10-year period. Developers need upfront financing to complete construction so they will usually sell their tax credits to outside investors (e.g., corporations, financial institutions) in exchange for equity financing. The equity reduces the financing developers would otherwise have to secure and allows tax credit properties to offer more affordable rents. Like the tax-exempt bonding authority, federal law caps the total tax credits that be awarded annually.

Finally, the Federal Home Loan Bank of San Francisco – an institution privately owned by financial institutions in the region of all sizes and many types – provides forgivable Affordable Housing Program (AHP), loans to projects meeting certain income and other criteria. AHP loans are awarded in funding rounds that can be competitive, and if a round is over-subscribed, developers will likely get smaller awards than they applied for. AHP awards average about $10,000 per unit.

Affordable housing developers receive a “developer fee” in lieu of making a profit on the project. The size the developer fee is generally set by either CDLAC or TCAC regulations. A deferred developer fee is, in effect, a loan to the project by the project sponsor that typically has priority over other soft money.

Further resources:

Congressional Research Service: An Introduction to the Low-Income Housing Tax Credit

SPUR: What We Talk About When We Talk About Affordable Housing: A Primer

Terner Center: The Cost of Building Housing