The Low-Income Housing Tax Credit (LIHTC) program has been one of the primary sources of federal support for affordable housing since its creation as part of the 1986 Tax Reform Act. LIHTC subsidizes the acquisition, construction, and rehabilitation of affordable rental housing for low- and moderate-income tenants.

How does LIHTC work?

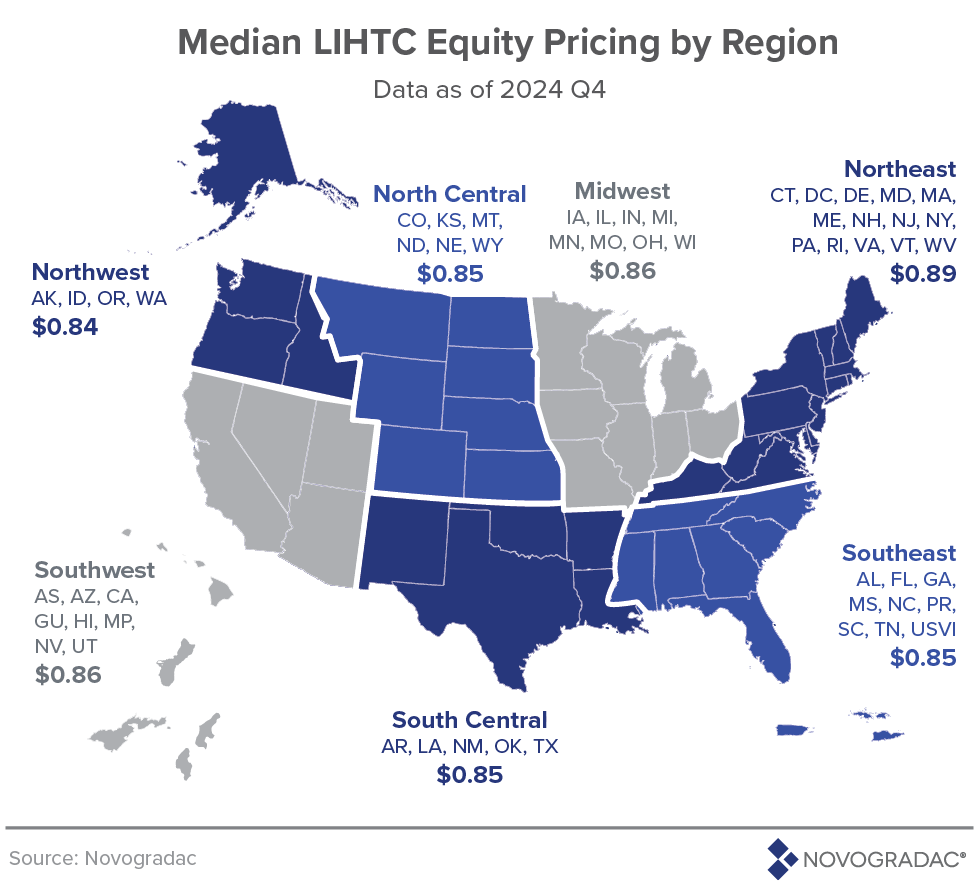

The federal government issues tax credits to state governments, which then award the credits to private developers of affordable rental housing through a competitive process. In California, the California Tax Credit Allocation Committee (CTCAC) sets competitive project scoring standards based on State priorities and awards LIHTCs. Once the tax credits are awarded, developers usually sell them to private investors and can use the money from the sale to pay for most project costs, except the cost of acquiring land. The price investors pay is less than the value of the tax credit (see map below), yielding a financial benefit for investors. Financial institutions are major investors because they have substantial income tax liabilities from real estate activities and receive Community Reinvestment Act (CRA) credit for these investments. Once the housing development is placed in service (made available to tenants), the federal tax code allows private investment in LIHTCs to be deducted from a corporation’s tax obligation over 10 years.

Tax credits are issued based on the eligible costs of an affordable development. The credits come in two varieties, known as 9% Credits and 4% Credits. The 9% Credits usually generate about 65% of the funds a development needs, and 4% Credits usually generate about 30% of the funds a development needs. The remaining financing for the development comes from several sources that must be assembled by the developer, usually a combination of bank loans, local loans and grants, and state funds. Once the various sources are assembled, these monies are collectively known as the “capital stack.”

The funds invested in affordable housing through LIHTCs are private, but Congress sets a limit on the amount of LIHTCs that can be allocated in any year since those credits represent tax revenue that will not be collected by the Treasury. In 2025, the fifty U.S. states received LIHTC allocations amounting to $3 per capita for the 9% LIHTC (small states receive a minimum allocation of $3,455,000 for the 9% LIHTC). The federal government provides much more support through the tax code for housing that is not targeted to low-income households—mostly through tax deductions for mortgage interest payments and property taxes.

The investors (or limited partners) in LIHTC developments usually play a passive role, receiving the tax benefits associated with the project but not participating in day-to-day management and oversight. The developer must comply with tax credit rules, including maintaining the lower-income rent restrictions, for 15 years (known as the “compliance period”). After that time, the investor typically exits the partnership, and the developer becomes the full owner. The State of California requires developers who receive LIHTCs to preserve the affordability of the development for a total of 55 years.

Not all developments that qualify for a LIHTC allocation receive it

Since the need for affordable housing is so great, demand for 9% Credits far surpasses the supply. CTCAC awards the Credits through a competitive process twice per year. Projects compete on point scoring. Factors that determine scores in the competitive process include the depth of affordability proposed, population served, proximity to transit, proximity to full-service grocery stores, and proximity to other resources such as schools and parks. However, because developers design projects in ways that earn the maximum score, CTCAC’s tiebreaker formula generally decides the outcomes. In 2023, the tiebreaker formula generally prioritizes developments with greater public benefits.

4% Credits are awarded automatically to projects receiving an allocation of tax-exempt private activity bonds from the California Debt Limit Allocation Committee (CDLAC). While there is no direct competitive process for receiving 4% Credits, there is a competitive process for receiving bond allocations, since there is not enough bond allocation available to meet the need for affordable housing.